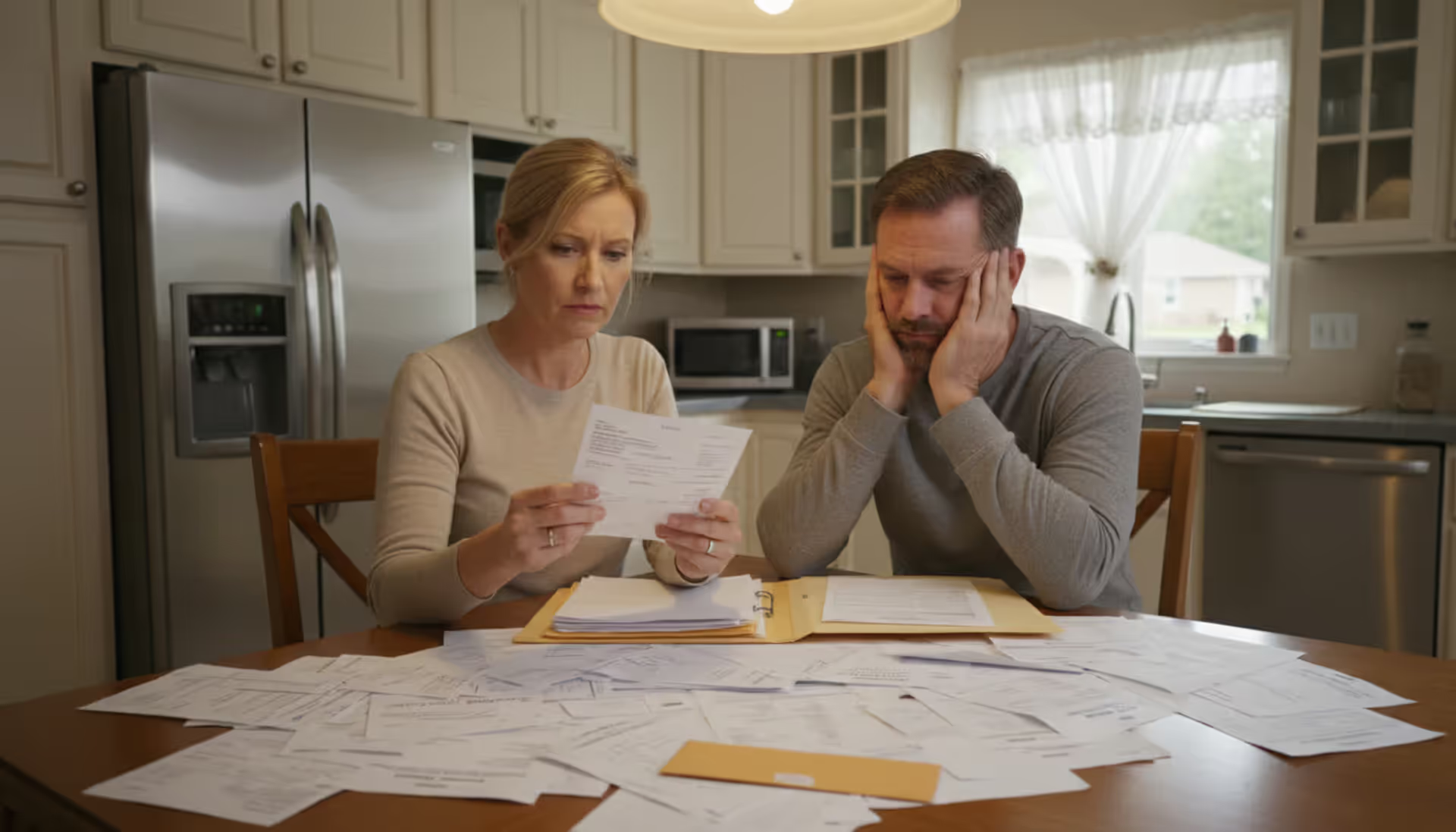

One trip to the emergency room changed everything for the Morrison family. What started as chest pain turned into triple bypass surgery—and a $187,000 hospital bill. Even with insurance, their out-of-pocket costs hit $34,000. Within six months, they'd drained their savings, maxed out three credit cards, and faced their first lawsuit from a collection agency.

Stories like this play out thousands of times daily across America. Healthcare costs don't just strain budgets—they destroy them. When you're staring at medical bills that would take a decade to repay, bankruptcy stops being a scary last resort. It becomes the only realistic path back to financial stability.

This guide walks through exactly how bankruptcy eliminates medical debt, which chapter fits your situation, and what the actual process looks like from start to finish.

What Medical Bankruptcy Is and How It Works

Here's something important right away: "medical bankruptcy" isn't its own legal category. You won't find it in the federal bankruptcy code. The term simply describes regular consumer bankruptcy—either Chapter 7 or Chapter 13—filed primarily because healthcare bills have buried you financially.

What is medical bankruptcy in practical terms? It's using existing bankruptcy law to wipe out hospital invoices, doctor bills, ambulance charges, and similar healthcare debts. These obligations fall under "general unsecured debt" in bankruptcy court, sitting in the same legal bucket as credit card balances or personal loans.

This categorization actually helps you. Unsecured debts rank below secured debts like mortgages in the priority order. They're also much easier to discharge than obligations like child support or recent tax debts, which bankruptcy can't touch.

The mechanics work one of two ways. Chapter 7 eliminates qualifying debts outright—usually within four months. Chapter 13 reorganizes what you owe into a manageable payment plan lasting three to five years. Either path activates something called the automatic stay immediately upon filing. This legal shield stops collection lawsuits cold, ends wage garnishments, and silences creditor phone calls.

Author: Ethan Calloway;

Source: dynamicrangemetering.com

Medical providers can't distinguish their bills from other unsecured debts during bankruptcy proceedings. That $4,000 emergency room charge gets identical treatment to a $4,000 Visa balance. No collateral backs these debts, and bankruptcy law makes no special provisions protecting medical creditors over credit card companies.

When Medical Debt Leads to Bankruptcy

Certain patterns emerge repeatedly in medical bankruptcy cases. Recognizing these situations helps you spot when bankruptcy shifts from theoretical option to practical necessity.

Uninsured patients face catastrophic exposure. Hospitals charge uninsured individuals full retail rates—often triple what insurance companies negotiate. A standard appendectomy might cost an insured patient $3,500 out-of-pocket. The same procedure bills an uninsured patient $22,000. One emergency creates decade-long debt.

High-deductible plans create a different trap. Your family might carry insurance with a $12,000 annual deductible. A cancer diagnosis in February means you'll hit that maximum quickly. But if treatment extends into January, the deductible resets. Suddenly you're facing $24,000 in out-of-pocket costs across two calendar years for one illness.

Catastrophic health events deliver a financial double-punch. Cancer treatment doesn't just generate $200,000 in medical bills—it also eliminates your income during six months of chemotherapy. Your employer might terminate you during extended leave, wiping out both your paycheck and health coverage simultaneously. Bills multiply while income disappears.

Medical debt also fragments uniquely. That three-day hospital stay generates separate invoices from the hospital facility, your primary physician, the consulting cardiologist, the anesthesiologist, the radiologist interpreting your scans, the lab processing bloodwork, and the medical equipment company renting you a heart monitor. You're juggling eight different creditors with eight payment demands from one hospital visit.

Collection lawsuits mark the point of no return for many people. Medical providers frequently sell unpaid accounts to collection agencies after 90-180 days. These agencies file lawsuits aggressively. Once a court issues a judgment, creditors gain legal authority to garnish your wages, levy bank accounts, and attach liens to property. How medical debt leads to bankruptcy often traces directly to this escalation from billing disputes to court judgments threatening your basic financial survival.

Chapter 7 vs. Chapter 13 for Medical Bills

Choosing your bankruptcy chapter shapes everything—timeline, costs, what you keep, what you pay. Here's how they compare for handling medical bills and bankruptcy discharge:

Feature

Chapter 7

Chapter 13

Eligibility

Income must fall below state median OR demonstrate limited disposable income through calculations

Requires steady income source; total debts can't exceed $2,750,000 combined secured and unsecured (2026 limit)

Four to six months from petition to final discharge

Three to five years making plan payments before discharge

Debt Discharge

Medical bills eliminated completely with zero payment

Partial payment on medical debt (typically 10–50% depending on income), remainder discharged after plan completion

Asset Protection

Trustee may liquidate assets exceeding exemption limits

Retain all property while making regular plan payments

Credit Impact

Stays on credit reports for 10 years from filing date

Stays on credit reports for 7 years from filing date

Chapter 7 Bankruptcy and Medical Debt Discharge

Chapter 7 delivers the fastest knockout punch to medical debt bankruptcy chapter 7 style. This liquidation approach wipes out qualifying debts in four to six months without requiring any repayment. Medical bills receive complete discharge because healthcare debt almost never qualifies for the narrow exceptions to discharge.

Eligibility hinges on passing the means test. Household income below your state's median for your family size? You're in automatically. Earn more than the median? You'll calculate disposable income using IRS expense standards. The formula subtracts allowed living expenses from your income. Failing this test doesn't automatically disqualify you—it just means the trustee might challenge your filing or suggest Chapter 13 instead.

Author: Ethan Calloway;

Source: dynamicrangemetering.com

Chapter 7 makes most sense when you own limited assets. Exemption laws protect certain property from liquidation. Federal exemptions typically cover $27,900 in home equity, $4,450 in vehicle equity, and unlimited retirement accounts (2026 figures). Non-exempt property—like a second car worth $15,000 or a valuable coin collection—could be sold by the trustee to pay creditors. Most Chapter 7 filings are "no-asset cases" where filers keep everything because it's all exempt.

Medical debt gets treated identically to credit card balances in Chapter 7. The court doesn't prioritize hospital debt bankruptcy discharge differently than other unsecured obligations. Whether you owe $8,000 or $800,000 in medical bills makes no difference legally—both amounts discharge completely.

Chapter 13 Payment Plans for Medical Bills

Chapter 13 reorganizes your debts into a court-supervised repayment plan spanning 36 to 60 months. Monthly payments are calculated based on your disposable income after subtracting necessary living expenses. This option works for people earning regular paychecks who want to protect non-exempt assets or whose income disqualifies them from Chapter 7.

Your payment plan prioritizes secured creditors first—meaning mortgage and car loans get paid in full. Whatever disposable income remains gets distributed among unsecured creditors, including medical providers. These unsecured creditors frequently collect pennies on the dollar. A family earning $55,000 annually might pay just 15% of unsecured debts through their plan.

Chapter 13 offers strategic benefits despite the longer commitment. You can cure mortgage arrears over five years while keeping your home. Car loan defaults get remedied through the plan. The automatic stay protection continues for the entire three-to-five-year period, preventing collection activity throughout. Medical creditors cannot contact you, sue you, or garnish wages while you're making plan payments.

Understanding bankruptcy for medical bills options through Chapter 13 requires knowing about the final discharge. After completing all plan payments, any remaining medical debt vanishes. If your plan paid 20% to unsecured creditors, the other 80% of your medical bills gets discharged exactly like Chapter 7—gone permanently.

How Filing Bankruptcy Clears Medical Debt

Let's answer the critical question directly: does bankruptcy clear medical debt? Yes—completely and permanently in almost all situations.

Hospital bills, physician charges, surgeon fees, diagnostic imaging costs, prescription copayments, ambulance transport, durable medical equipment rentals, physical therapy—all qualify as general unsecured debt eligible for discharge. Bankruptcy eliminates these obligations whether you file Chapter 7 or complete a Chapter 13 plan.

Author: Ethan Calloway;

Source: dynamicrangemetering.com

The discharge order operates as a permanent federal court injunction. Once the judge issues it, medical creditors legally cannot pursue collection through any means—no lawsuits, no phone calls, no collection letters, no negative credit reporting. Creditors violating discharge protections face contempt charges, financial penalties, and potential liability for damages to you.

Certain medical-related obligations require careful handling. Bills incurred after filing your bankruptcy petition don't receive discharge because they weren't included in your case. Debts obtained fraudulently—like falsely claiming insurance coverage to receive treatment—might be challenged as non-dischargeable. Personal injury restitution ordered by criminal courts survives bankruptcy, though standard medical malpractice settlements typically discharge.

Secured medical debts follow different rules. Occasionally medical providers require security agreements for expensive treatments or medical equipment. These secured debts work like car loans—you must either surrender the collateral, pay the secured amount in full, or redeem the property by paying its current fair market value.

The automatic stay begins protecting you instantly when your petition hits the court's electronic filing system. Active wage garnishments must stop within days. Bank account freezes get released. Pending lawsuits get halted mid-litigation. Collection agencies must cease contact immediately upon receiving bankruptcy notice—no grace period, no exceptions.

Medical bills and bankruptcy discharge include all associated collection costs. If a hospital sued you and obtained a $15,000 judgment that included $4,000 in attorney fees and court costs, bankruptcy discharges the entire $19,000. You're not liable for any collection expenses, legal fees, or interest charges that accrued before filing.

The Medical Bankruptcy Filing Process Step-by-Step

Filing bankruptcy for medical debt process follows a specific sequence with mandatory deadlines. Here's what actually happens:

Credit counseling requirement: You must complete an approved credit counseling session within 180 days before filing. These run 60-90 minutes, typically cost $10-$50, and are available online. The agency issues a completion certificate that gets filed with your bankruptcy petition. No certificate means no bankruptcy filing—period. Both Chapter 7 and Chapter 13 require this step with zero exceptions.

Document gathering: Assemble six months of pay stubs, your last two years of tax returns, recent bank statements, deeds for real property, vehicle titles, and comprehensive lists detailing every debt and asset you own. For medical debt documentation, gather itemized hospital bills, explanation of benefits forms from your insurer, and collection letters. Missing documents delay processing and potentially trigger case dismissal.

Means test completion: Chapter 7 requires official means test forms comparing your household income against your state's median. Calculations use a six-month lookback period, averaging income during that window. Some income doesn't count—Social Security benefits, for instance—which might help you qualify despite seemingly high total income.

Petition filing: Your attorney prepares the bankruptcy petition, schedules of assets and debts, and supporting documentation, then files everything with the bankruptcy court. Chapter 7 filing fees ($338 in 2026) must be paid upfront. Chapter 13 fees ($313) can be paid in installments. Most courts require electronic filing, with your petition entering the system immediately.

Automatic stay activation: Protection begins the instant your petition is filed—not when creditors receive notice, not after court review, but immediately. This federal injunction stops nearly all collection activity instantly. Medical providers must halt collection efforts the moment they receive bankruptcy notification.

Meeting of creditors: Between 21-40 days post-filing, you'll attend the 341 meeting conducted by your bankruptcy trustee. This happens in an office conference room, not a courtroom. Expect questions about your financial situation, assets, and debts while under oath. Medical creditors can attend and question you but rarely do—most 341 meetings last 10-15 minutes with only the trustee present.

Financial management course: Before discharge, you must complete a debtor education course covering budgeting and money management. This second required course is separate from pre-filing credit counseling. Expect to pay $15-$50. Chapter 7 filers must complete this within 60 days after the 341 meeting.

Discharge order: Chapter 7 filers typically receive discharge orders 90-120 days after filing, assuming no complications. Chapter 13 filers receive discharge only after making all required plan payments—three to five years post-filing. The discharge order officially eliminates qualifying debts and closes your case.

Author: Ethan Calloway;

Source: dynamicrangemetering.com

Costs and Consequences of Medical Bankruptcy

Bankruptcy delivers powerful debt relief, but you're trading current debt for future consequences. Understanding the full cost picture helps you weigh bankruptcy against alternatives.

Court filing fees represent your smallest expense. Chapter 7 costs $338 while Chapter 13 runs $313. Chapter 7 filers earning below 150% of federal poverty guidelines can request fee waivers, though hiring an attorney typically disqualifies you from waiver approval.

Attorney fees swing widely based on location and complexity. Simple Chapter 7 cases in smaller markets might run $1,500 total. Complex Chapter 13 cases in major metropolitan areas can exceed $6,000. Many bankruptcy attorneys accept payment plans. Chapter 13 attorney fees can be incorporated into the repayment plan itself, meaning you pay the lawyer through monthly plan payments over time.

Your credit score takes an immediate, substantial hit. Expect drops of 130-200 points, though people with already-damaged credit see smaller decreases. Chapter 7 bankruptcy stays on credit reports for a decade from filing date. Chapter 13 remains for seven years. That said, many people rebuilding after medical bankruptcy qualify for secured credit cards within 12-18 months and car loans within two years of discharge.

Asset risks depend entirely on what you own and applicable exemption laws. Chapter 7 trustees liquidate non-exempt assets to generate funds for creditors. Federal exemptions protect $27,900 in home equity (2026), $4,450 in vehicle equity, and unlimited retirement accounts. State exemptions vary dramatically—Florida and Texas offer unlimited homestead protection, while other states protect only a few thousand dollars of home equity.

Employment impacts are generally minimal. Federal law prohibits government employers from bankruptcy discrimination. Private employers rarely check bankruptcy records. Security clearances present nuanced situations—while bankruptcy appears on background checks, resolving overwhelming debt through legal means often improves clearance prospects compared to ongoing financial chaos and delinquent accounts.

Consider alternatives before filing. Many hospitals, especially nonprofit facilities, maintain financial assistance programs that reduce or eliminate bills for low-income patients. Direct negotiation with medical providers often yields settlements at 30-50% of billed charges. State charity care programs provide another avenue for debt reduction without credit damage.

Medical debt drives nearly half of all personal bankruptcy filings in the United States, affecting more than 500,000 families annually. Unlike other forms of debt, medical bankruptcy often strikes people who were financially stable before a sudden health crisis upended their lives

— Rebecca Martinez

Frequently Asked Questions About Medical Bankruptcy

Does bankruptcy eliminate all medical bills?

Yes, bankruptcy discharges virtually every type of medical bill—hospital charges, physician fees, surgical costs, ambulance transport, medical equipment rentals, and prescription expenses. The narrow exceptions are debts obtained fraudulently or secured by specific collateral. Medical bills already reduced to court judgments discharge completely, eliminating both the original debt and added collection costs. Bills incurred after you file your bankruptcy petition receive no discharge because they weren't listed in your original case.

Can I file bankruptcy for medical debt alone?

Absolutely. Bankruptcy law imposes no minimum debt thresholds or requirements that you owe multiple debt types. People routinely file bankruptcy when medical bills represent their only significant financial problem—particularly after catastrophic illnesses generate six-figure charges. Remember though: bankruptcy appears on your credit report whether you discharge $10,000 or $500,000, so weigh the credit consequences against your total debt burden before filing.

Will I lose my home if I file medical bankruptcy?

Most people keep their homes using homestead exemptions that protect equity. Federal exemptions shield up to $27,900 in home equity (2026 amount), while state exemptions range from modest protection to unlimited in states like Florida and Texas. If your equity exceeds available exemptions, Chapter 13 lets you keep the home by paying the non-exempt equity value through your repayment plan over time. Chapter 7 trustees only sell homes when substantial equity exists after paying off mortgages and exemption amounts—and when the sale would actually benefit creditors.

How long does medical bankruptcy stay on my credit report?

Chapter 7 remains on your credit reports for 10 years measured from your filing date. Chapter 13 stays for seven years from filing. Individual medical debts included in bankruptcy should be updated to show "discharged in bankruptcy" with zero balance owed. Creditors sometimes fail to update their reporting correctly—you can dispute inaccuracies directly with credit bureaus. While the bankruptcy notation persists for years, its impact on your credit score diminishes significantly over time, especially as you establish new positive payment history.

What happens to medical bills in collections during bankruptcy?

Collection agencies must immediately stop all collection activity when they receive official notice of your bankruptcy filing. The automatic stay prohibits collection calls, demand letters, lawsuits, and negative credit reporting. Medical debts sold to collection agencies discharge identically to debts still held by original healthcare providers. Collectors violating the automatic stay or discharge injunction can be held in contempt of court—you can file motions seeking sanctions and damages. The bankruptcy trustee might also recover preferential payments made to collection agencies within 90 days before filing, though this rarely affects individual debtors.

Can medical debt be discharged in Chapter 13?

Chapter 13 absolutely discharges medical debt—specifically, whatever remains unpaid after completing your repayment plan. If your plan pays 25% to unsecured creditors over five years, the remaining 75% of medical bills receives a complete discharge identical to Chapter 7. Some Chapter 13 plans pay zero to unsecured creditors when all disposable income goes toward secured debts like mortgage arrears. Medical creditors cannot object to discharge simply because they received minimal payment—courts approve plans based on your income and necessary expenses, not creditor preferences.

Medical bankruptcy provides legitimate, legally-protected relief when healthcare costs exceed any reasonable ability to pay. Whether you pursue Chapter 7's quick elimination or Chapter 13's structured approach, bankruptcy law categorizes medical debt as dischargeable unsecured debt eligible for complete elimination.

Filing bankruptcy shouldn't be an automatic response to medical bills, though. The decision requires analyzing your complete financial picture, understanding available exemptions in your state, and considering long-term goals. Many hospitals offer payment plans or charity care programs that preserve your credit rating. But when medical bills exceed realistic repayment capacity, when creditors have secured judgments against you, or when garnishments threaten your ability to afford rent and groceries—bankruptcy provides a clear legal pathway forward.

Meeting with a bankruptcy attorney helps clarify how exemption laws apply to your specific assets, whether you qualify for Chapter 7 or should pursue Chapter 13, and what timeline and costs to expect. Most bankruptcy attorneys provide free initial consultations where they review your situation and explain options without any commitment required.

Medical bankruptcy isn't a character flaw—it's a legal tool Congress created specifically to give honest people crushed by circumstances beyond their control a genuine opportunity to rebuild financially. Understanding the actual process, costs, and outcomes empowers you to make informed decisions about your financial future rather than drowning in debt that a medical emergency created through no fault of your own.

Bankruptcy stays on credit reports for 7-10 years, but errors happen frequently. Discover how to identify bankruptcy reporting mistakes, dispute inaccurate information with credit bureaus, and rebuild your credit score through proven strategies after bankruptcy discharge

Bankruptcy remains on your credit report for 7-10 years depending on the chapter filed, but its impact diminishes significantly over time. Understanding the specific timeline and taking strategic rebuilding steps helps you recover your credit score and qualify for loans years before the bankruptcy notation disappears

Filing for bankruptcy triggers significant credit consequences, but understanding the specific impact helps you prepare and recover. Chapter 7 stays on your report for 10 years and can drop scores 150-240 points, while Chapter 13 remains for 7 years with a 130-200 point decrease

Tax debt can feel overwhelming, especially when the IRS begins collection actions. Bankruptcy can eliminate certain tax debts under specific conditions, but not all tax obligations qualify for discharge. Understanding the 3-year, 2-year, and 240-day rules is essential for determining eligibility

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to bankruptcy, debt relief, credit rebuilding, and related legal processes.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Bankruptcy outcomes and procedures may vary depending on jurisdiction, personal circumstances, and applicable laws.

This website does not provide legal, financial, or credit advice, and the information presented should not be used as a substitute for consultation with qualified attorneys or financial advisors.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.