Filing bankruptcy in America feels like someone stamped "financial failure" across your forehead. Here's what most people don't realize: that stamp fades faster than you think, and creditors are surprisingly eager to work with you again—often within months of your discharge. The timeline isn't mysterious. Commit to specific rebuilding tactics, and you'll likely hit a 650-680 score in roughly two years. Push to 720+ within four to five years if you're disciplined.

You're actually starting from an advantage most struggling borrowers don't have: zero debt. While bankruptcy tanks your score initially, you're not juggling collections, charge-offs, and maxed cards anymore. Clean slate. Lenders recognize this, which is why entire product categories exist specifically for your situation.

The challenge isn't whether you can rebuild credit post-bankruptcy—it's whether you'll follow the unglamorous, repetitive habits that make it happen.

Understanding Your Credit Situation After Bankruptcy

Right after discharge, expect your score to land somewhere between 500 and 550. That's the typical range. If you filed with a 720 score, the 200-point plunge feels catastrophic. Someone who filed with a 580 score experiences a smaller drop—maybe 30-80 points—because their credit was already battered.

The Chapter 7 vs. Chapter 13 distinction affects your timeline differently than most people expect. Chapter 7 (liquidation bankruptcy) stays visible on your Equifax, Experian, and TransUnion reports for a full decade from your filing date. Chapter 13 (reorganization with a repayment plan) disappears after seven years. Sounds like Chapter 13 is the better option for your credit, right? Not necessarily.

Here's the twist: Chapter 7 filers often rebuild faster in practice. Why? Because they're done. Discharged. They can immediately start adding positive tradelines. Chapter 13 borrowers spend 3-5 years making court-ordered payments, during which they're technically still "in bankruptcy" and heavily restricted from taking on new credit. Some creditors view the Chapter 13 repayment commitment favorably, but most consumers find the immediate freedom of Chapter 7 allows quicker recovery.

One underappreciated benefit: bankruptcy wipes out the individual negative marks from your pre-filing disasters. Those five collection accounts showing 180 days late? That charged-off credit card? All gone. Yes, the bankruptcy notation itself is severe, but you're no longer accumulating damage from multiple delinquent accounts. Your report actually looks cleaner than it did six months before filing, which creates a workable foundation for becoming creditworthy after bankruptcy.

Developing a credit improvement plan after bankruptcy isn't complicated—it just requires accepting you'll spend 18-36 months proving you've changed your financial behavior.

Timeline: How Long Does It Take to Rebuild Credit After Bankruptcy

Let's get specific about what "rebuilding" actually looks like at each stage:

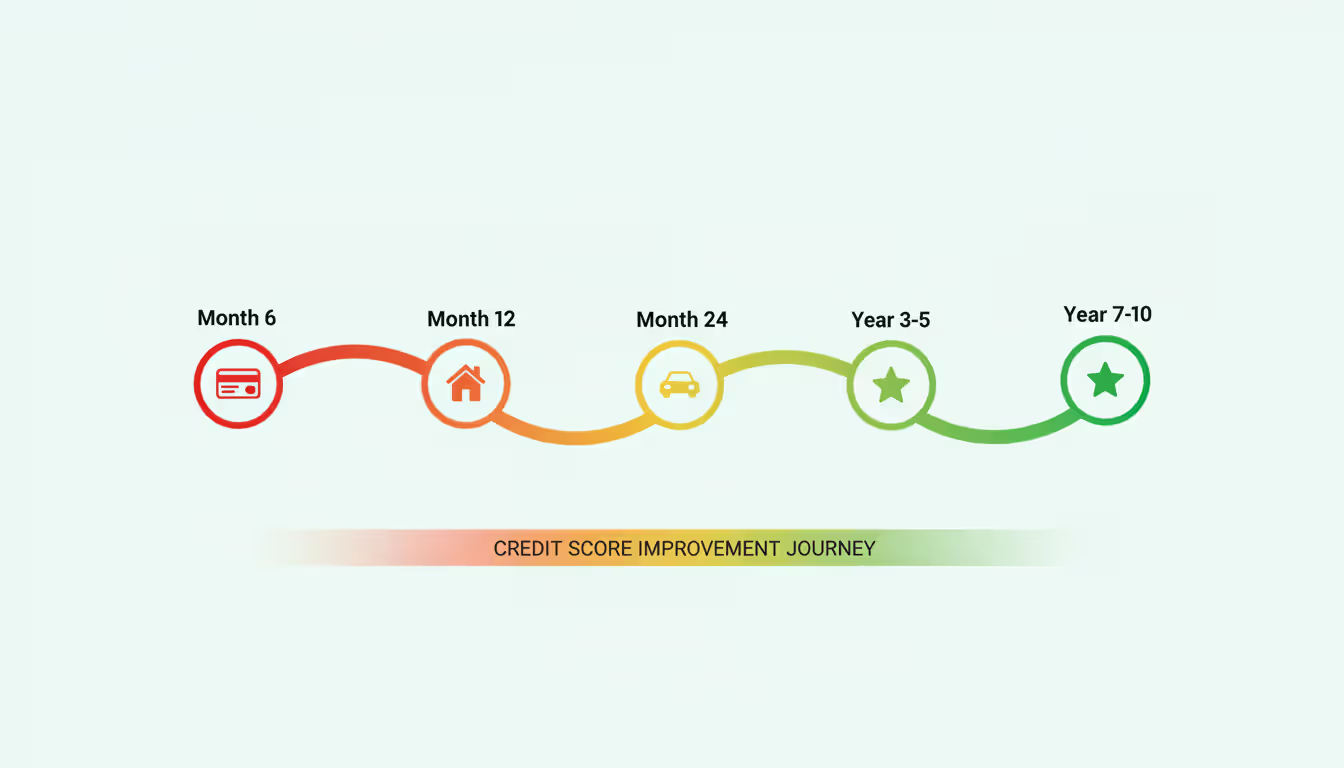

Months 1-6: You're probably sitting at 520-590. Expect incremental improvements of 10-30 points as you add one or two accounts and establish perfect payment history. This is your window to apply for a secured card (more on that shortly) and possibly start a credit builder loan. Don't expect dramatic jumps—you're building a foundation.

Month 12: Disciplined filers typically land between 600 and 650 by their one-year anniversary. You've demonstrated a full year of on-time payments across maybe two or three accounts. Credit card companies start sending pre-qualified offers again (though the terms still aren't great—think 24.99% APR and $500 limits). Subprime auto lenders will approve you, albeit at interest rates in the 14-18% range.

Month 24: The 650-700 zone becomes realistic. This milestone matters because many landlords, utility companies, and insurance providers use 650 as a cutoff. FHA mortgages become accessible at the two-year mark after Chapter 7 discharge, assuming you've maintained spotless payment history. Your secured cards may have graduated to unsecured by now, refunding your deposits.

Years 3-5: Breaking 700 is achievable for consistent borrowers. The bankruptcy still appears on your report, but credit scoring algorithms weight recent positive behavior more heavily than old negative events. Conventional mortgages typically require four years distance from bankruptcy discharge. Prime auto loans with single-digit interest rates become available. You're competing on nearly equal footing with people who never filed.

Year 7-10: Chapter 13 bankruptcies fall off at seven years. Chapter 7 at ten years. By this point, assuming you've maintained good habits, your score should match someone with similar credit characteristics who never filed bankruptcy.

What accelerates this timeline? Keeping utilization below 10% (not 30%), diversifying your credit mix early, and obsessively protecting your payment history. What slows everything down? A single 30-day late payment in month 14 can erase six months of progress. Maxing out your new credit cards signals you haven't learned impulse control. Applying for six different cards in three months makes lenders think you're desperate.

The best way to rebuild credit after bankruptcy guide isn't sexy: it's boringly consistent payments on a small number of accounts for 24-36 months straight.

Author: Samantha Crowley;

Source: dynamicrangemetering.com

Secured Credit Cards: Your First Step to Credit Recovery

Think of a secured card as a credit card with training wheels. You hand the bank $300, $500, or sometimes $1,000. That deposit becomes your spending limit, and it sits in an account as collateral. You charge purchases like any credit card. The difference? If you disappear without paying, the bank keeps your deposit. Zero risk for them, maximum opportunity for you to demonstrate responsible usage.

Here's the rebuilding mechanism: the issuer reports your payment activity to all three credit bureaus. Charge $50, pay $50, repeat monthly. Within 90 days, you've got three on-time payment notations across all three reports. That's gold when you're rebuilding.

Most issuers approve bankruptcy filers between one and three months post-discharge. Some accept applications immediately. Others make you wait 6-12 months. Your deposit comes back eventually—either when you close the account with a zero balance, or when the issuer upgrades you to an unsecured card (usually after 12-18 months of perfect payments).

Your secured credit card after bankruptcy strategy has three objectives: establish reliable payment history, maintain utilization below 10%, and graduate to unsecured status within 18 months.

Here's a tactical approach: charge one recurring subscription (Netflix, Spotify, whatever) to the card. Set up autopay from your checking account to pay the full statement balance every month. Never touch the card otherwise. This creates consistent reporting with zero mental effort and zero risk of overspending.

The interest rate doesn't matter if you're following this approach—you're never carrying a balance. Yes, secured cards typically charge 22-28% APR, but you'll pay $0 in interest by paying the full balance monthly. Building credit doesn't require paying interest. That's a myth.

Choosing the Right Secured Card After Bankruptcy

Not all secured cards help you rebuild effectively. Focus on these criteria:

Three-bureau reporting: Verify the issuer reports to Equifax, Experian, and TransUnion. Incredibly, some secured cards only report to one or two bureaus, which handicaps your rebuilding. Call and confirm before applying.

Upgrade pathway: The top-tier secured cards automatically review your account every 6-8 months for graduation to unsecured status. You want this feature. When you graduate, your deposit gets refunded automatically, your credit line often increases, and you've successfully transitioned to traditional credit. Cards without graduation paths keep you in secured status indefinitely.

Minimal fees: Annual fees between $0 and $35 are reasonable. Anything above $50 is excessive. Run away from cards charging monthly maintenance fees ($6.95/month adds up to $83.40/year for no reason), application fees, or "processing charges." These exist to extract money from people rebuilding credit—they provide zero value.

Reasonable deposit minimums: Most cards require $200-$500 to start. Some allow deposits up to $5,000. Here's the thing: a $5,000 deposit doesn't rebuild credit five times faster than $500. Don't tie up more cash than necessary. Start with $300-$500, use the card responsibly, and graduate to unsecured within a year.

A useful feature some secured cards offer: the ability to add to your deposit later to increase your credit limit. If you deposit $300 initially (giving you a $300 limit) and later need more spending room, you can add another $200 to reach $500. This avoids applying for new credit just to get higher limits.

Common Mistakes to Avoid With Secured Cards

Opening three secured cards simultaneously screams desperation to lenders. Each application generates a hard inquiry. Three inquiries in one week for secured cards—when one would suffice—suggests poor judgment. Start with one card. Use it properly for 6-8 months. Then consider adding a second if you genuinely need additional tradelines.

People rush to close their secured card the moment they get their deposit refunded after graduation. Bad move. That card is now your oldest post-bankruptcy account. Closing it erases that history and lowers your average account age—both hurt your score. Keep the graduated card open. Use it once every 3-4 months for a small purchase, pay it off, done.

Treating your deposit as available money creates problems. That $400 sitting with the card issuer isn't accessible for emergencies while the account is active. Budget as if that money doesn't exist. Only deposit amounts you can afford to have locked away for 12-18 months.

Author: Samantha Crowley;

Source: dynamicrangemetering.com

Credit Builder Loans and Alternative Credit-Building Tools

Credit builder loans flip traditional lending upside down. Normal loans: bank gives you $5,000, you repay it over time. Credit builder loan: bank deposits $1,000 into a locked savings account or CD, you make monthly payments for 12-24 months, and when you're done, you get the $1,000. The bank reports every payment to the bureaus.

Why would anyone do this? Because you're building credit while forcing yourself to save. The loan payment (typically $25-$75 monthly) becomes mandatory savings. You can't access the money until the loan is paid off, at which point you receive a lump sum. It's a savings account with credit-building benefits attached.

Interest rates run between 6% and 12%, which seems counterintuitive—you're paying interest to access your own money later. Think of the interest as the fee for the credit-building service. On a $1,000 loan at 10% over 24 months, you'll pay roughly $100 in interest but receive $1,000 at the end. You're essentially paying $100 to add 24 months of positive installment loan history to your credit report.

Credit builder loan after bankruptcy works particularly well because it adds installment loan diversity to complement your secured card (revolving credit). Credit scoring models reward account diversity.

Community banks and credit unions offer better credit builder loan terms than most online lenders. Navy Federal, Alliant Credit Union, and local community banks frequently have programs starting at $25/month. Online services like Self and Credit Strong specialize in these products but charge higher fees. Compare before committing.

Becoming an authorized user on someone else's credit card can boost your score, but it's risky and you need to be selective. If your mother has a 15-year-old credit card with a $10,000 limit, 8% utilization, and has never missed a payment, being added as an authorized user can instantly add that positive history to your report. Some scoring models count this fully; others discount authorized user status.

The danger: if the primary cardholder starts missing payments or maxes out the card, it damages your credit too. You're along for the ride, good or bad. Only pursue this with someone who has impeccable credit habits and whom you trust completely. And have an honest conversation first—they need to understand that their mistakes will hurt you.

Rent and utility reporting services like Experian Boost, RentTrack, or LevelCredit add alternative payment data to your credit file. You connect your bank account, and they verify you've paid rent and utilities on time. This data shows up on your credit report and can provide a modest score boost—typically 10-30 points.

The catch: FICO scoring models don't weight rent and utilities as heavily as credit cards and loans. VantageScore considers them more seriously. Still, when you have limited tradelines in the first 6-12 months post-bankruptcy, every positive notation helps. These services usually charge $5-$15 monthly, which is reasonable if you're trying to hit a specific score threshold for an apartment or insurance policy.

Self-lender products bundle credit builder loans with CDs. You make payments that go into a certificate of deposit, earning a small amount of interest (maybe 1-2%). The lender reports your payments. When the term ends, you receive your savings plus the interest earned. It's one of the cleaner credit rebuilding strategies post bankruptcy because it combines credit building, forced savings, and a guaranteed return.

Essential Habits for Rebuilding Credit Quickly

Payment history is 35% of your FICO score—the single largest component. Miss one payment by 30 days, and you'll watch your score drop 60-100 points. When you're rebuilding, you can't afford this. Set up automatic payments for at least the minimum due on every account. Even if you plan to manually pay more later in the billing cycle, the autopay is your safety net against forgetfulness, travel, or chaos.

Credit utilization represents 30% of your score. The formula: total balances divided by total credit limits. If you have two cards with $500 limits each ($1,000 total available credit) and you're carrying $300 in balances, your utilization is 30%. That's the maximum you should carry, but under 10% is significantly better for scoring purposes.

Practical tactic: if your secured card has a $500 limit, keep the reported balance under $50. How? Either pay the card down multiple times throughout the month before the statement cuts, or just use it for small charges. The balance reported to bureaus is typically your statement balance, not your current balance. Pay down big charges before the statement closes.

Mixing credit types (revolving accounts like credit cards, plus installment loans like auto loans or credit builder loans) helps your score. The credit mix category is only 10% of FICO, but it matters. You don't need five different account types—a secured card plus a credit builder loan gives you both categories covered. That's sufficient when you're rebuilding credit after bankruptcy steps guide.

Hard inquiries ding your score by 3-5 points each and remain visible for two years (though they only affect your score for 12 months). Be strategic with applications. Don't apply to six different credit cards "just to see" if you'll get approved. Each decline comes with an inquiry and no benefit. Research which issuers approve post-bankruptcy filers, then apply to one at a time.

There's an exception: rate shopping for auto loans or mortgages. Multiple inquiries for the same loan type within a 14-45 day window (depending on the scoring model) count as a single inquiry. The system recognizes you're shopping for rates, not desperately seeking credit everywhere.

Author: Samantha Crowley;

Source: dynamicrangemetering.com

Check your credit reports every 90 days through AnnualCreditReport.com (the only genuinely free, federally authorized source). Post-bankruptcy reports frequently contain errors. Discharged debts still showing balances. Accounts marked "charged off" instead of "discharged in bankruptcy." Incorrect bankruptcy filing dates. Each error suppresses your score unnecessarily. Dispute immediately through the bureau's website—not through third-party services.

Budgeting prevents the missed payments that destroy rebuilding progress. This isn't exciting advice, but it's essential. If taking on a $35/month credit builder loan payment means you'll occasionally skip your phone bill, don't do it. Your rebuilding timeline depends entirely on consistent, on-time payments across every obligation. Build your budget first, then add credit products you can afford.

How to improve credit after bankruptcy isn't about gaming the system—it's about demonstrating month after month that you've become financially reliable.

What Not to Do When Rebuilding Credit Post-Bankruptcy

The biggest self-sabotage I see is bankruptcy filers who wait 18 months before taking any action because they're embarrassed or think they need to 'lay low.Then they have a bankruptcy on their report with zero positive payment history to counterbalance it. You need to start rebuilding within 30-60 days. Get that secured card immediately, make small purchases, pay in full monthly. Clients who follow this consistently typically reach 680-720 scores within three years. Those who wait two years before starting often take five or six years to reach the same point

— Jennifer Martinez

Applying for excessive credit too quickly raises red flags with lenders. You get approved for a secured card, then immediately apply for three more secured cards, two credit builder loans, and a retail store card. Lenders reviewing your file see someone who learned nothing from bankruptcy and is desperate to access credit again. Space your applications 4-6 months apart minimum.

Closing accounts with zero balances seems logical but hurts you in two ways. First, it reduces your total available credit, which increases your utilization percentage on remaining cards. If you have $1,000 available credit and close a card with a $500 limit, you now have $500 available—your utilization just doubled. Second, closing accounts lowers your average account age, especially if you're closing your oldest post-bankruptcy card.

Exception: if a card charges a $95 annual fee and you're not using it, closing makes financial sense. But if there's no annual fee? Keep it open. Charge something small every 3-4 months so the issuer doesn't close it for inactivity.

Credit repair companies promising to remove bankruptcy from your report are running scams. Accurate information cannot be legally removed before the statutory timeframe—seven years for Chapter 13, ten years for Chapter 7. These companies charge $50-$150 monthly to send dispute letters you could file yourself for free. They cannot deliver on their promises. Save your money.

The credit repair industry preys on people desperate for quick fixes. The only legitimate credit repair is correcting actual errors on your report, which you can do yourself through the bureau's dispute process. No company has special access or secret strategies to remove accurate negative information.

Missing payments on your new credit accounts is catastrophic for rebuilding. You've spent six months establishing perfect payment history, building your score from 540 to 610. Then life gets chaotic and you miss your secured card payment by 30 days. That single missed payment can drop your score 80-100 points instantly, erasing half a year of progress. Protect your payment history obsessively.

Maxing out new credit demonstrates you haven't learned spending discipline. If you're approved for a $500 secured card and immediately charge $500, you're signaling poor money management to lenders. They gave you credit to test your behavior—maxing it out fails the test. Keep your balances low relative to limits, ideally under $100 per $500 in credit.

Co-signing loans for friends or family puts your rebuilding at risk. You're legally responsible if they don't pay. Their late payments become your late payments. Their default becomes your default. The answer is no—regardless of who's asking or what sob story accompanies the request—until your credit is fully rebuilt and you can absorb a potential disaster. Usually, that means waiting 3-5 years post-bankruptcy.

Comparison of Credit-Building Products After Bankruptcy

Product

Typical Cost

Time to Impact Credit

Approval Difficulty

Pros

Cons

Secured Credit Card

$200-$500 deposit plus $0-$49 yearly fee

Starts reporting immediately; noticeable score impact within 90-180 days

Easy; most issuers approve 30-90 days post-discharge

Builds revolving credit history; potential graduation to unsecured within 12-18 months; flexible spending

Requires cash deposit that's locked away; interest rates typically 22-28% if you carry balances

Credit Builder Loan

6-12% interest on loan amounts from $300-$1,000

Starts reporting immediately; noticeable score impact within 90-180 days

Moderate; some credit unions require 3-6 month waiting period post-bankruptcy

Builds installment loan history; forced savings mechanism; money returned at end of term

Cash locked during 12-24 month term; paying interest to access your own money; fixed monthly payment required

Authorized User Status

Free if added by friend/family

Can be immediate if account has long history; impact varies by scoring model

Depends entirely on primary cardholder's willingness and credit quality

No cost; no application; can add years of positive history instantly

Zero control; primary holder's mistakes damage your credit; some lenders ignore authorized user tradelines

Frequently Asked Questions About Credit After Bankruptcy

Can I get a credit card immediately after bankruptcy discharge?

Yes, and you probably should. Secured credit card issuers specifically target post-bankruptcy consumers because the deposit eliminates their risk. Most approve applications within 30-60 days of discharge. You'll need to provide your discharge paperwork and proof of income. Wait about two weeks after your discharge date to ensure it's processed in court systems, then apply. Capital One, Discover, and OpenSky are among issuers known for approving recent bankruptcy filers.

Will paying off old debts improve my credit after bankruptcy?

No, not if those debts were included in your bankruptcy discharge. Once discharged, those accounts should show zero balance owed and be marked "included in bankruptcy" or "discharged." Paying them doesn't remove the bankruptcy notation and provides no credit score benefit—you're giving away money for nothing. The exception: if you reaffirmed a debt during bankruptcy (keeping your car loan or mortgage by agreeing to keep paying it), then yes, continuing timely payments helps your score because that account wasn't discharged.

Should I work with a credit repair company after bankruptcy?

No. What credit repair companies do—send dispute letters to credit bureaus—you can do yourself for free through each bureau's website. They cannot remove accurate information like bankruptcy, and they can't speed up the seven- or ten-year reporting period. Legitimate credit counseling through non-profit agencies like NFCC or Money Management International offers free budget counseling and education. That's useful. But for-profit credit repair companies charging monthly fees almost never deliver value worth the cost.

How many credit accounts should I open after bankruptcy?

Start with one secured credit card within 60 days of discharge. Use it responsibly for 6-9 months. Then consider adding either a second secured card or a credit builder loan around the 9-12 month mark. By 18-24 months post-bankruptcy, having 2-3 accounts in perfect standing is sufficient for solid rebuilding. More accounts don't accelerate your progress and create more opportunities for mistakes. Quality and consistency matter more than quantity.

Can I get a mortgage or car loan while rebuilding credit after bankruptcy?

Auto loans become available 12-18 months post-bankruptcy through subprime and specialty lenders, though expect interest rates between 12% and 19%. FHA mortgages are accessible two years after Chapter 7 discharge (or one year into a Chapter 13 repayment plan with court permission). Conventional mortgages typically require four years post-discharge plus credit scores above 620. VA loans require two years post-discharge for veterans. Your score, down payment size, income stability, and post-bankruptcy payment history all factor into approval decisions and interest rates.

Does bankruptcy ever come off my credit report?

Yes, automatically. Chapter 13 bankruptcies disappear seven years from your filing date—not discharge date, filing date. Chapter 7 bankruptcies disappear ten years from filing. The credit bureaus remove these entries automatically when the time expires; you don't need to request removal or take any action. However, the practical impact on your score starts declining significantly after 24-36 months of positive credit behavior, so you won't need to wait the full period to qualify for most credit products at reasonable terms.

Rebuilding credit after bankruptcy isn't complicated—it's just unglamorous and requires patience you may not feel like exercising. The timeline is approximately 24-36 months to reach good credit (680-720 range), and four to five years to achieve excellent credit above 740. Achievable? Absolutely. Quick? No.

Your bankruptcy eliminated crushing debt, which gave you something most struggling borrowers don't have: financial breathing room. You're not juggling collection calls and spiraling balances anymore. Use that clean slate strategically by establishing positive payment history immediately, keeping your credit utilization below 10%, and avoiding the impulsive financial decisions that created problems originally.

A secured credit card and a credit builder loan provide the structural foundation. Disciplined payment habits across all obligations—rent, utilities, phone service, insurance—demonstrate creditworthiness month by month. The work is repetitive. Pay everything on time, every time, for 24 months straight. That's the entire strategy.

Check your credit reports quarterly through AnnualCreditReport.com and dispute any errors immediately. Celebrate small milestones: your first 620 score, graduating from secured to unsecured card status, hitting 700. Each milestone represents genuine financial progress and brings you closer to competitive lending terms.

The credit system absolutely allows second chances for people who demonstrate changed behavior through consistent actions. Your bankruptcy doesn't determine your financial future five years from now—your actions during the next 24-36 months do. Start rebuilding this month, not next year. By the time three years pass, you'll have the credit profile needed for prime interest rates and legitimate financial opportunities.

Filing for bankruptcy offers immediate relief from crushing debt, but it triggers a cascade of consequences that ripple through your financial life for years. Understanding these effects—from credit damage to employment hurdles—helps you weigh whether bankruptcy is the right solution

Filing for bankruptcy marks the end of one financial chapter and the beginning of another. This comprehensive guide covers everything from immediate post-filing steps to long-term credit rebuilding strategies, helping you understand discharge timelines, avoid common pitfalls, and create a sustainable financial plan

Facing overwhelming debt? Understanding the differences between debt consolidation and bankruptcy helps you choose the right relief strategy. Consolidation reorganizes debt into manageable payments, while bankruptcy can eliminate it entirely through legal proceedings. Each option carries distinct costs and consequences

Federal law sets no lifetime limit on bankruptcy filings, but mandatory waiting periods restrict how often you can file. Chapter 7 requires eight years between discharges, while Chapter 13 permits refiling after two years. Understanding these rules and good faith requirements is essential for successful refiling

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to bankruptcy, debt relief, credit rebuilding, and related legal processes.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Bankruptcy outcomes and procedures may vary depending on jurisdiction, personal circumstances, and applicable laws.

This website does not provide legal, financial, or credit advice, and the information presented should not be used as a substitute for consultation with qualified attorneys or financial advisors.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.