Person standing at a crossroads between a dark broken path and a bright clear road leading toward sunlight on the horizon with scattered documents on the ground

When you file for bankruptcy, you get relief from overwhelming debt—but your credit report tells that story for years to come. The bankruptcy mark doesn't vanish overnight, and different filing types leave different timelines behind.

Here's what surprises most people: your credit doesn't stay ruined forever. Far from it. Within a few years of filing, many people qualify for car loans, credit cards, and even home mortgages. The bankruptcy notation sits on your report for a set period, but lenders care less about it as time passes and you prove your financial reliability.

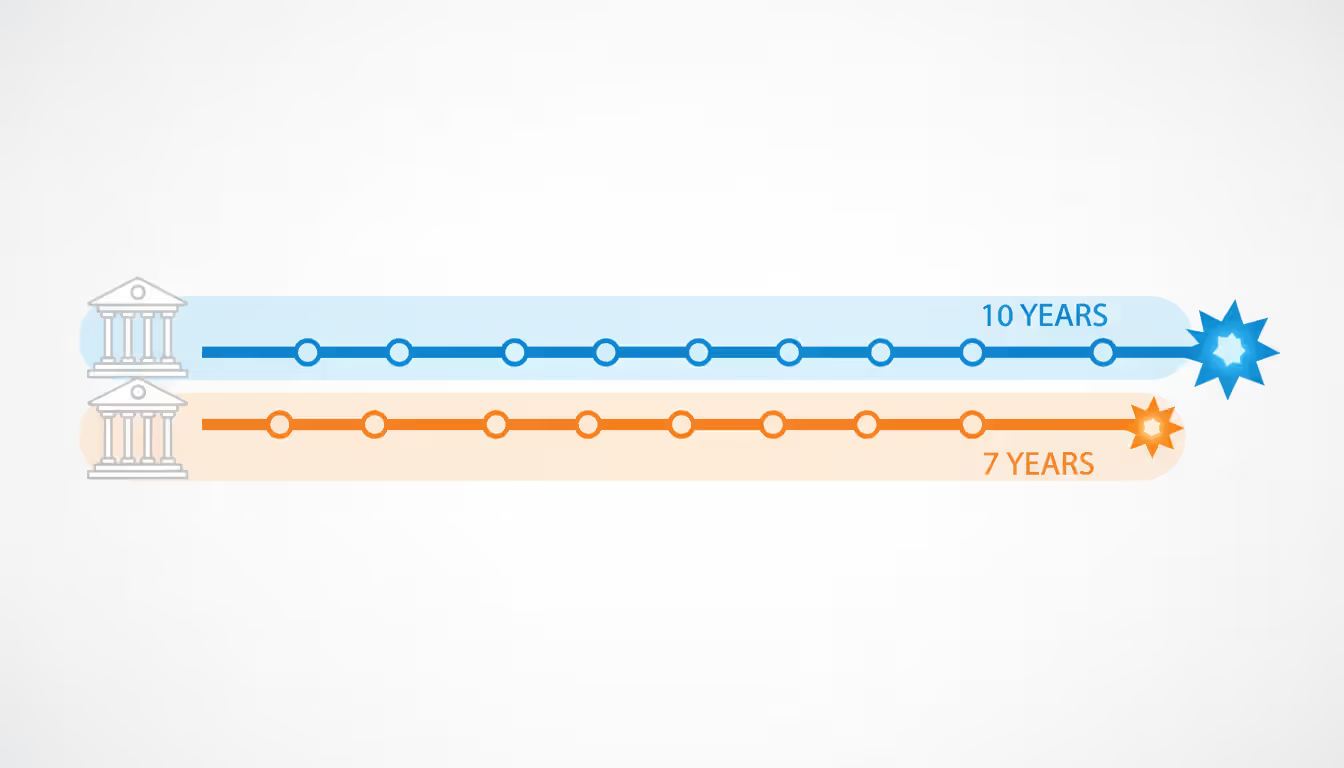

The type of bankruptcy you choose—Chapter 7 or Chapter 13—determines exactly how many years you'll see it listed when someone pulls your credit.

Bankruptcy Reporting Periods by Type

Federal law through the Fair Credit Reporting Act establishes maximum timeframes for bankruptcy listings. These aren't suggestions—they're legally binding limits on how long this information can appear.

Chapter 7 filings stick around for a full decade, counting from the date you submitted your petition to the court. This version liquidates your qualifying assets to settle with creditors, then wipes away most remaining unsecured balances. You'll typically walk away debt-free within four to six months. Because you're eliminating debts rather than repaying them, the credit bureaus can list this filing for 10 years.

Chapter 13 cases remain visible for seven years after your filing date. You're committing to a repayment plan lasting three to five years, during which you pay back at least some portion of what you owe. Since you're making an effort to repay creditors through court supervision, the bankruptcy credit history duration complete is shorter by three years.

Author: Ethan Calloway;

Source: dynamicrangemetering.com

Your filing date starts the countdown—not when the court grants your discharge. File Chapter 7 on April 10, 2024? It vanishes from credit reports on April 10, 2034. Choose Chapter 13 on that same date, and removal happens April 10, 2031.

Individual accounts wrapped into your bankruptcy follow their own rules. A credit card debt discharged in bankruptcy might fall off seven years from when you first missed payments, which could be earlier than the bankruptcy notation itself disappears. This staggered removal means some negative items vanish while the bankruptcy filing remains visible.

Here's how many years bankruptcy on record affects you based on filing type:

Factor

Chapter 7

Chapter 13

Credit Report Duration

10 years after filing

7 years after filing

Eligibility Requirements

Income means test; below state median or limited disposable income

Rebuilding your credit beautifully doesn't shorten the bankruptcy on record duration total. Even someone who reaches an 800 credit score will still see the bankruptcy listed until the prescribed timeframe expires.

How Bankruptcy Affects Your Borrowing Over Time

How long bankruptcy affects borrowing follows a predictable downward slope. The worst damage concentrates in the first 24 months. Traditional lenders mostly refuse applications during this window, and the few willing to extend credit charge interest rates that would make you wince.

Years one and two after filing look like this: - Secured credit cards requiring cash deposits become your primary option - Auto financing exists but costs 8–15 percentage points above what prime borrowers pay - Personal loans are scarce, and those available carry heavy fees - Conventional home mortgages remain out of reach

The bankruptcy credit timeline complete improves noticeably during years three and four. Lenders start weighing your recent payment behavior more heavily than that bankruptcy notation. If you've paid every bill on time and built some positive credit history: - Unsecured credit cards start arriving in your mailbox (with modest $500–$1,500 limits initially) - Auto loan rates drop to just 4–8 points above prime - FHA mortgages become possible (Chapter 7 filers can apply two years after discharge with 3.5% down) - Personal loan approval odds increase substantially

Years five through seven mark when bankruptcy stops affecting you for most practical lending decisions. Creditors still see the filing when pulling your report, but your recent track record matters more. Many institutions use internal policies that greenlight applicants whose bankruptcy occurred five-plus years ago, assuming everything else checks out.

Once you cross the seven-year threshold for Chapter 13 (or the ten-year mark for Chapter 7), the notation drops off entirely. However, some loan applications—especially for mortgages—include questions like "Have you filed bankruptcy in the past seven years?" You'll need to answer truthfully even if it's no longer on your credit file.

Credit scores bounce back faster than you'd expect. Someone starting at 720 pre-bankruptcy might crater to 530 immediately after filing. With disciplined rebuilding efforts: - 12 months later: 530–580 - 24 months later: 580–620 - 36 months later: 620–660 - 48 months later: 660–690 - 60 months later: 690–720

Author: Ethan Calloway;

Source: dynamicrangemetering.com

These estimates assume you're making every payment on time, keeping credit card balances under 10% of limits, and avoiding new negative marks. Your specific results depend on your pre-bankruptcy credit profile and how aggressively you tackle rebuilding.

When Bankruptcy Is Removed from Your Credit Report

Equifax, Experian, and TransUnion should automatically purge bankruptcy filings once the legal reporting window closes. The credit bureau bankruptcy timeline complete relies on automated systems programmed to flag and delete items based on dates.

Reality doesn't always match theory. Studies suggest 15–20% of consumers discover their bankruptcy still showing up after the deadline passes because of database errors, wrong dates in the system, or technical glitches.

Pull reports from all three bureaus right when you hit the 7-year mark (Chapter 13 filers) or 10-year mark (Chapter 7 filers). You can access free weekly reports at AnnualCreditReport.com. Spot the bankruptcy still listed past its expiration? Time to dispute.

Disputing works through these steps:

Submit disputes to each bureau currently showing the expired bankruptcy

Attach documentation proving your filing date—discharge papers from the court work perfectly

Write clearly: "I filed this bankruptcy on, meaning the legal reporting period ended on under FCRA regulations"

Bureaus get 30 days to investigate and respond

Most legitimate disputes about how long until bankruptcy removed from record resolve within that first 30-day investigation. The bureau verifies your filing date against court records, confirms the reporting period has expired, and deletes the entry.

Sometimes bankruptcy records show incorrect filing dates—perhaps a data entry mistake lists your May 2015 filing as May 2016, tacking on an extra year. This happens more frequently with Chapter 13 cases involving years of payments and multiple court interactions that create data confusion.

The three major credit bureaus operate independently. One might delete the bankruptcy right on schedule while another requires you to dispute. This creates frustrating situations where a lender checking Experian sees your bankruptcy while another pulling from Equifax doesn't.

Court records themselves never disappear. After bankruptcy drops from credit reports, the public filing still exists in federal court databases accessible through PACER. Employers, landlords, or others conducting deep background checks might uncover old bankruptcies through court searches rather than credit reports.

Author: Ethan Calloway;

Source: dynamicrangemetering.com

Rebuilding Credit After Bankruptcy

Strategic rebuilding accelerates your recovery and shrinks how long bankruptcy affects borrowing in practical, real-world terms. You're not just marking time—you're actively proving you've learned from past financial struggles.

Secured credit cards offer the quickest path forward. Deposit $200–500 with the card issuer, receive a card with that amount as your credit limit, then make small purchases you pay off completely each month. This generates positive payment history immediately. Many issuers convert these to regular unsecured cards after 12–18 months of spotless payments, then return your deposit.

Look for secured cards reporting to all three bureaus and charging reasonable fees. Annual fees above $50 or monthly maintenance charges signal predatory products targeting desperate consumers.

Credit-builder loans flip traditional lending backward. The lender puts your "loan amount" into a savings account they control. You make monthly payments for 12–24 months, building payment history with each one. When the term ends, you receive the money. These make sense if you can handle the monthly commitment and want to add installment loan history to your credit mix.

Becoming an authorized user on someone else's well-managed card can boost your score within weeks. Their entire payment history for that account appears on your credit report. This requires finding someone—often a financially responsible parent or sibling—who trusts you and maintains excellent credit habits.

Credit history after bankruptcy years improves fastest when you maintain: - Balances below 10% of your credit limits (not just the commonly cited 30%) - Perfect payment timing on every single obligation - A combination of revolving credit (cards) and installment loans (car, personal) - Few hard inquiries from limiting applications to genuinely necessary credit

Realistic timelines for major credit milestones post-bankruptcy: - Secured credit card: Available immediately after discharge - Unsecured credit card: 12–24 months - Auto loan at competitive rates: 24–36 months - FHA mortgage: 24 months after Chapter 7 discharge; 12 months into Chapter 13 plan - Conventional mortgage: 48 months post-discharge - Credit score breaking 700: 36–60 months with disciplined rebuilding

Resist opening multiple accounts quickly. Every application creates a hard inquiry temporarily dinging your score. More critically, lenders view numerous recent accounts as risky behavior—especially from someone with bankruptcy history.

Author: Ethan Calloway;

Source: dynamicrangemetering.com

Common Mistakes That Extend Bankruptcy's Impact

The bankruptcy notation follows a fixed timeline, but poor choices after filing can extend the practical damage years beyond when it drops off your report.

Missing payments after bankruptcy causes the worst damage. One single payment 30 days late during year two of your recovery can slash your score by 60–80 points and tells lenders you haven't changed your financial habits. Creditors specifically scrutinize post-bankruptcy payment patterns. Perfect payments demonstrate you've learned and grown; scattered late payments suggest the same old problems persist.

Automate at least minimum payments on every obligation. The psychological relief from bankruptcy discharge sometimes creates false confidence leading to sloppy payment habits.

Applying for excessive credit immediately triggers multiple problems. Each application generates a hard inquiry dropping your score 2–5 points for two years. More importantly, numerous recent accounts make you appear desperate or financially unstable. Lenders might deny applications based solely on too many recent inquiries, regardless of your actual score.

Better approach: get one secured card right after discharge, add a second credit product after 12 months of perfect payments, then space additional applications at least six months apart.

Skipping credit report monitoring means errors, fraud, or identity theft goes unnoticed for months. Bankruptcy filers face elevated identity theft risk—criminals assume you're not watching closely. Check reports from all three bureaus every three months. Watch for: - Accounts you never opened - Wrong bankruptcy filing dates extending the timeline - Discharged debts still showing balances owed - Incorrect late payment marks on post-bankruptcy accounts you paid promptly

Closing old accounts that survived bankruptcy damages your credit age and utilization ratio. If you kept a credit card through bankruptcy—perhaps one where you owed nothing—keep it active with small recurring charges paid automatically. Account age factors into credit scoring, and older accounts provide substantial benefit.

Falling for credit repair scams wastes hundreds or thousands of dollars. Companies promising to remove accurate bankruptcy information are lying—legally reported bankruptcies can't be erased early, period. Legitimate credit repair involves disputing genuine errors and building positive history, which you can handle yourself at no cost.

Some bankruptcy filers accumulate fresh debt too quickly after discharge, creating financial stress without having bankruptcy as a safety net (you typically can't file Chapter 7 again for eight years). Discharge eliminates existing debts but doesn't fix underlying spending patterns or income shortfalls.

Bankruptcy is a legal proceeding in which you put your money in your pants pocket and give your coat to your creditors

— Joey Adams

Frequently Asked Questions About Bankruptcy and Credit History

Does bankruptcy ever completely disappear from my record?

After seven years for Chapter 13 or ten years for Chapter 7, bankruptcy vanishes from credit reports maintained by Equifax, Experian, and TransUnion. Credit bureaus legally can't report it beyond those timeframes. However, the public court record documenting your bankruptcy filing remains permanently searchable through federal court databases. Most lenders only check credit reports rather than court records, so the practical impact ends when it leaves your credit file. Some mortgage applications ask "Have you ever filed for bankruptcy protection?" requiring honest disclosure even decades later when it's long gone from credit reports.

Can I get a mortgage before bankruptcy falls off my credit?

Absolutely—mortgage approval happens well before the bankruptcy notation disappears. FHA loans become available 24 months after receiving a Chapter 7 discharge, or just 12 months into a Chapter 13 repayment plan if you're making on-time payments and get court permission. VA loans for veterans require waiting two years from discharge. Conventional mortgages typically demand a four-year waiting period post-discharge plus credit scores around 620–640. You'll need documented stable income, solid employment history, and a down payment—often 10–20% for conventional loans, just 3.5% for FHA. Expect interest rates slightly above prime rates until your bankruptcy ages past five years.

Will bankruptcy show up on background checks for employment?

Bankruptcy appears on credit reports, which some employers review during hiring—particularly for positions in financial services or roles involving cash handling. Beyond credit reports, bankruptcy constitutes a public court record anyone can search through PACER, the federal court database. Employers checking credit need your written authorization under Fair Credit Reporting Act rules. They must notify you if credit information influences their hiring decision, giving you opportunity to explain circumstances. Bankruptcy alone rarely disqualifies candidates unless the job involves significant financial management responsibilities or requires security clearance.

Does paying off debts early remove bankruptcy faster?

No—the bankruptcy reporting period is locked by federal law based on when you filed, regardless of how quickly you complete the process or whether you voluntarily repay discharged debts. Chapter 7 remains ten years from filing even though discharge typically happens within months. Chapter 13 stays seven years from filing even if you finish your repayment plan in three years rather than five. Voluntarily repaying discharged debts doesn't affect the timeline and generally makes no financial sense—those debts are legally eliminated. Focus your energy on building fresh positive credit history, which improves your score much faster than the notation's eventual removal.

How do the three credit bureaus handle bankruptcy differently?

Equifax, Experian, and TransUnion receive bankruptcy data from court records and theoretically should report identically, but discrepancies happen regularly. One bureau might list an incorrect filing date while others show accurate information. The bankruptcy might appear under different sections—public records versus derogatory marks—depending on the bureau. Individual accounts included in your bankruptcy may report differently across bureaus based on how each creditor reports the discharge. Always check all three reports rather than assuming one represents what the others show. Disputing errors requires separate disputes with each bureau displaying incorrect information. Since lenders pull from different bureaus, inconsistent reporting can mean approval from one lender and denial from another for identical loan applications.

Can I dispute a bankruptcy on my credit report?

You can dispute bankruptcy only when the information contains inaccuracies or exceeds legal reporting timeframes. Valid dispute reasons include: incorrect filing date, wrong bankruptcy chapter listed, bankruptcy belonging to someone else with a similar name, or bankruptcy still appearing after seven years (Chapter 13) or ten years (Chapter 7). You cannot dispute accurately reported bankruptcy simply because you want it removed sooner—that's not how the system works. File disputes directly with credit bureaus online, by mail, or by phone, including documentation supporting your claim like court discharge papers. Frivolous disputes attempting to remove accurate information get rejected quickly and waste time better spent actively rebuilding credit.

Your credit report carries a bankruptcy notation for seven to ten years depending on which chapter you file, but the practical impact on your financial life diminishes far more quickly. The listing itself follows a rigid timeline, yet your ability to borrow and qualify for competitive rates can recover within two to four years through strategic credit rebuilding and consistent financial management.

Knowing the specific reporting periods, automatic removal processes, and recovery timelines lets you plan realistically rather than assuming permanent damage. Chapter 7 stays visible for ten full years while Chapter 13 disappears after seven. Neither timeline shortens based on your rebuilding success, but lenders increasingly overlook older bankruptcy filings when recent payment history demonstrates reliability and growth.

Minimizing bankruptcy's long-term impact requires action, not passive waiting for the notation to vanish. Immediately establishing fresh positive credit patterns makes all the difference. Secured credit cards, credit-builder loans, and authorized user status provide accessible rebuilding tools. Combined with perfect payment timing and minimal credit utilization, these strategies can restore your score to good or excellent levels years before the bankruptcy notation finally drops off.

Steer clear of common pitfalls that extend the damage: missed post-bankruptcy payments, excessive credit applications triggering multiple hard inquiries, and ignoring credit report errors that could be disputed. Monitor your reports regularly across all three bureaus, dispute inaccuracies promptly, and maintain the financial discipline preventing future credit problems.

When the reporting period expires, verify removal across Equifax, Experian, and TransUnion, then dispute any lingering notations. The bankruptcy filing remains searchable in court records indefinitely, but its absence from credit reports marks the end of its influence on most lending decisions. Your credit future depends far more on the positive history you build during recovery than on the bankruptcy mark itself.

Filing for bankruptcy offers immediate relief from crushing debt, but it triggers a cascade of consequences that ripple through your financial life for years. Understanding these effects—from credit damage to employment hurdles—helps you weigh whether bankruptcy is the right solution

Filing for bankruptcy marks the end of one financial chapter and the beginning of another. This comprehensive guide covers everything from immediate post-filing steps to long-term credit rebuilding strategies, helping you understand discharge timelines, avoid common pitfalls, and create a sustainable financial plan

Facing overwhelming debt? Understanding the differences between debt consolidation and bankruptcy helps you choose the right relief strategy. Consolidation reorganizes debt into manageable payments, while bankruptcy can eliminate it entirely through legal proceedings. Each option carries distinct costs and consequences

Bankruptcy doesn't mean permanent credit damage. Most filers reach fair credit within 18-24 months using secured cards, credit builder loans, and consistent payment habits. This guide covers timelines, products, and strategies to rebuild creditworthiness after Chapter 7 or Chapter 13 discharge

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to bankruptcy, debt relief, credit rebuilding, and related legal processes.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Bankruptcy outcomes and procedures may vary depending on jurisdiction, personal circumstances, and applicable laws.

This website does not provide legal, financial, or credit advice, and the information presented should not be used as a substitute for consultation with qualified attorneys or financial advisors.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.