Filing bankruptcy overwhelms most people—until they understand what actually happens to their debts. Here's the reality: discharge serves as the legal mechanism erasing your personal obligation to repay certain debts. Without obtaining this discharge, you'd gain almost nothing from bankruptcy except a temporary pause from collection calls.

Most bankruptcy filers want exactly one thing: discharge. How long the process takes varies based on whether you file Chapter 7 or 13, which debts you're carrying, and whether you finish every mandatory step. After the court grants discharge, many debts vanish from your legal obligations. Others? They stick around no matter what.

What Is a Bankruptcy Discharge?

Think of the discharge as your official court document erasing the legal requirement to repay eligible debts. This isn't just paperwork—it's a permanent judicial order. Lenders can't call you, send collection letters, garnish wages, or sue you for those balances. Ever.

Here's something people get confused about: the debt itself doesn't disappear. Your responsibility to pay it does. The creditor still has records showing you owed $15,000 on that credit card. But you're freed from any legal duty to pay it back. They'll mark it as a loss and move on.

When someone mentions they're a "discharged bankrupt," they've completed the entire process and received final relief. The bankruptcy itself appears on credit reports for years afterward, but the active case? Finished.

Breaking down how the discharge order actually works: it functions like a shield. Federal law prohibits creditors from attempting collection on eliminated debts. This protection—bankruptcy courts call it the discharge injunction—never expires for covered debts. If a lender ignores your discharge and demands payment anyway, you can ask the bankruptcy court to penalize them. Courts don't tolerate these violations.

One crucial limitation: only debts you had before filing get this protection. Rack up new bills after you submit your bankruptcy petition? You owe those in full. The law prevents people from going on spending sprees right before filing, knowing the charges would get wiped out.

Author: Victor Langston;

Source: dynamicrangemetering.com

How the Debt Discharge Process Works in Bankruptcy

Several checkpoints stand between your initial filing and final discharge. Miss one checkpoint, and you could lose your discharge entirely.

You'll start by filing extensive paperwork documenting every debt, asset, income stream, and monthly expense. A court-appointed trustee scrutinizes everything for accuracy and completeness. Credit counseling must happen within 180 days before you file—no way around this timing requirement. After filing but before discharge, you'll need a financial management course. Both are mandatory—no exceptions.

Your creditors get notified immediately after you file. This triggers the automatic stay, which stops most collection actions cold. Creditors can file claims stating what you owe them. Meanwhile, your trustee examines whether you own property that should be sold to pay creditors. Most Chapter 7 cases don't involve selling anything, though.

The trustee serves as a neutral administrator checking your compliance with bankruptcy rules. You'll attend a 341 meeting (named after the bankruptcy code section requiring it) where you answer financial questions under oath. Assuming the trustee finds no problems and creditors don't object, the court issues your discharge months later.

Once the court issues your discharge order, creditors receive immediate notification through the court's electronic filing system, preventing them from pursuing any further collection on eliminated debts.

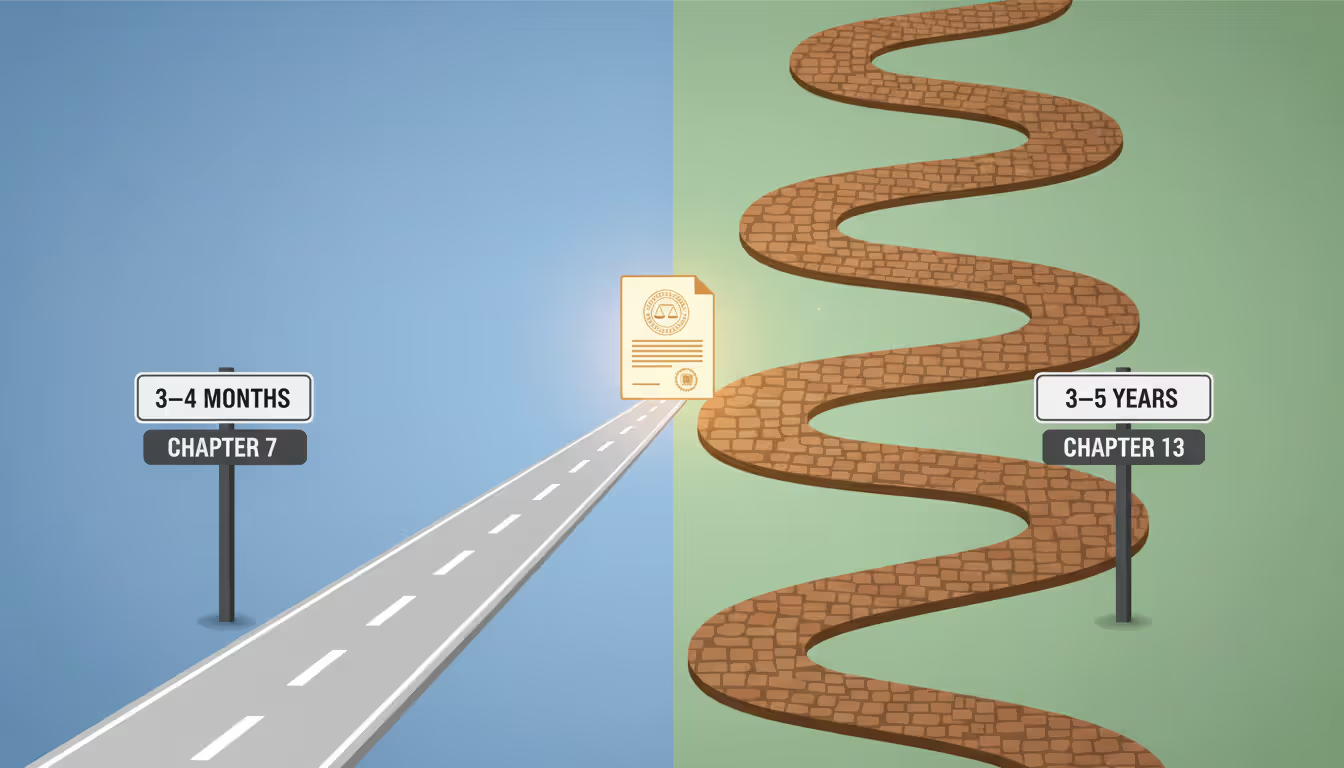

Chapter 7 Discharge Timeline

Chapter 7 moves faster than other bankruptcy chapters. Expect your discharge roughly three to four months post-filing. Here's the typical sequence:

Filing your petition activates immediate automatic stay protections. Within 20 to 40 days, you'll attend the 341 creditors' meeting. After that meeting concludes, a 60-day window opens during which creditors can object to your discharge or challenge specific debts. If nobody objects and you've finished your financial management course, expect discharge around day 90 to 120.

People carrying mostly unsecured debts with limited income find Chapter 7 particularly effective. The entire case usually wraps up within four to six months, making it the fastest route to discharge.

Problems extend these timeframes significantly. Creditors challenging your discharge, starting adversary proceedings, or trustees discovering hidden assets? Your case might drag on for many additional months. Missing deadlines for required paperwork or courses postpones discharge until you comply.

Chapter 13 Discharge Timeline

Chapter 13 operates on a much longer timeline because you must complete a three-to-five-year repayment plan first. You won't get immediate debt relief—instead, you'll make monthly payments to your trustee, who pays creditors according to your court-approved plan.

Discharge arrives only after you've made every required plan payment. Three-year plans mean waiting roughly 36 months from filing. Five-year plans? You're looking at 60 months. You'll also need to verify you're current on child support or alimony, plus complete the financial management course before the court grants discharge.

The extended Chapter 13 timeline offers a major benefit: it eliminates certain debts that survive Chapter 7. Some tax debts, property settlement obligations from divorce, and other categories can be discharged through Chapter 13 after completing your plan. This makes the longer wait worthwhile for people needing to eliminate these specific balances.

Chapter 13 also lets you catch up on mortgage arrears and car loan defaults through your plan, helping you keep property you might lose in Chapter 7. Your final discharge covers not just debts paid through the plan but also many unsecured debts that received little or no payment.

Which Debts Are Eliminated by Bankruptcy Discharge?

Understanding which obligations actually get erased requires knowing bankruptcy's specific rules. Not everything qualifies for elimination, and some debts survive regardless of which chapter you choose.

Dischargeable debts include most unsecured balances: credit card charges, medical bills, personal loans, utility arrears, past-due rent, business debts from sole proprietorships, and civil judgments—though judgments from fraud or intentional harm won't qualify. These obligations disappear completely after discharge, assuming creditors don't successfully challenge them.

Mortgages and car loans create different issues since they're secured by property. Discharge eliminates your personal liability for the debt, but the lender's security interest in collateral remains. Planning to keep your house or vehicle? You'll need to keep making payments. Surrender the property instead? Discharge prevents the lender from chasing you for any remaining deficiency after they sell it.

Non-dischargeable debts survive bankruptcy. These include most student loans (covered separately below), recent tax debts (typically under three years old), child support and alimony, debts incurred through fraud, obligations from intentional injuries you caused, government fines and penalties, and any debts you forgot to list in your bankruptcy filing.

Type of Debt

Discharged in Chapter 7?

Discharged in Chapter 13?

Credit card balances

Yes

Yes

Medical bills

Yes

Yes

Personal loans

Yes

Yes

Student loans

Rarely (separate lawsuit required)

Rarely (separate lawsuit required)

Income taxes under 3 years old

No

No

Income taxes over 3 years old

Usually

Usually

Child support or alimony

No

No

Court-ordered fines and penalties

No

No

Debts from fraudulent activity

No

No

Personal liability on secured loans

Yes

Yes

HOA fees before filing

Yes

Sometimes

Debts from DUI-related injuries

No

No

Some debts fall into unclear territory. HOA fees you owed before filing can be discharged, while fees accruing after filing cannot. Tax penalties older than three years might qualify if their underlying tax debt also qualifies. Property settlement debts from divorce can't be discharged in Chapter 7 but might be in Chapter 13.

Creditors can fight whether specific debts should be discharged by filing an adversary proceeding—basically a lawsuit within your bankruptcy case. They must prove you created the debt fraudulently, took out cash advances right before filing, or committed other violations. If they win, that particular debt survives your bankruptcy even though other debts get eliminated.

When Is Bankruptcy Discharged?

Timing matters significantly in bankruptcy. When you actually receive discharge depends on which chapter you filed, how quickly you complete requirements, and whether complications arise.

Chapter 7 cases typically end with discharge around the 90 to 120-day mark post-filing when everything proceeds smoothly. Court rules prohibit granting discharge until at least 60 days after your 341 meeting, giving creditors adequate time to object. You must complete your financial management course before this window closes, or discharge gets delayed until you comply.

Author: Victor Langston;

Source: dynamicrangemetering.com

After you finish all plan payments and submit required certifications, you'll receive your Chapter 13 discharge—a process taking anywhere from three to five years depending on your specific plan's duration. Courts won't grant early discharge even if you want to accelerate payments, unless you've paid 100% of every allowed claim.

Several factors push discharge past standard timeframes. Failing to submit mandatory documents—tax returns, pay stubs, bank statements—allows trustees to request dismissal or delay your discharge. Creditor challenges require court hearings that add months to the process. When the U.S. Trustee's office suspects fraud or abuse, they may file motions delaying discharge while investigating.

Forgetting the financial management course represents the most common preventable delay. Many people complete their pre-filing credit counseling but forget about the post-filing requirement. Without this second certificate, courts cannot issue discharge. Some courts automatically close cases when you miss this deadline, forcing you to file motions to reopen and pay additional fees.

Discharge hearings themselves are mostly administrative. Unlike the 341 meeting, you typically won't attend a separate discharge hearing. Courts simply issue written discharge orders mailed to you and every creditor. Some districts schedule brief hearings when creditors have objected or unusual circumstances exist, but most discharges get granted without hearings.

What Happens After Bankruptcy Discharge?

Life after receiving your discharge order involves both immediate changes and long-term adjustments. Understanding these shifts helps you avoid mistakes during this critical recovery phase.

Credit reports will show the bankruptcy for seven years (Chapter 13) or ten years (Chapter 7) starting from your filing date. Individual accounts included in bankruptcy should display notations like "included in bankruptcy" or "discharged" with zero balances. Creditors can't continue reporting these accounts as delinquent after discharge.

You can start rebuilding credit immediately after discharge. Secured credit cards become available, requiring deposits but reporting to credit bureaus like regular cards. Some credit card companies specifically target recent bankruptcy filers with high-interest products. Yes, the terms are expensive, but responsible use—keeping balances low and paying on time—helps reconstruct your credit profile.

Credit scores typically plummet when filing bankruptcy, often dropping 200 points or more. However, if your credit was already damaged through late payments, collections, and maxed-out cards before filing, bankruptcy itself might not drop your score much further. Many people see scores beginning to recover within 12 to 18 months after discharge, especially when they establish new positive payment histories.

Author: Victor Langston;

Source: dynamicrangemetering.com

The discharge injunction permanently blocks creditors from pursuing discharged debts. When a creditor calls, writes, or sues you about a discharged debt, they're violating federal law. You can ask the bankruptcy court to hold them in contempt, potentially recovering damages plus attorney fees.

Some creditors make mistakes, continuing to send bills or reporting discharged debts as active on credit reports. Document every violation, send cease-and-desist letters citing your bankruptcy case number and discharge date, and consult your bankruptcy attorney if the creditor persists. Courts treat discharge violations seriously and impose sanctions on creditors who ignore discharge orders.

Reaffirmation agreements complicate the post-discharge landscape. Signing a reaffirmation agreement for a car loan or mortgage during bankruptcy means that debt survives discharge. You remain personally liable for reaffirmed debts exactly as if you never filed bankruptcy. This means the creditor can repossess or foreclose if you default, and can pursue you for any deficiency balance.

Some people mistakenly believe they must reaffirm debts to keep property. Not necessarily true. You can often keep property by simply maintaining payments, even without reaffirming. Only sign reaffirmation agreements after careful consideration, as they remove the protection your discharge would otherwise provide.

Your tax refunds after discharge generally belong to you, though timing creates different outcomes. Chapter 7 filers expecting tax refunds for their filing year might see trustees claim those refunds as bankruptcy estate assets. Refunds for tax years after your filing date belong entirely to you. Chapter 13 filers may need to surrender tax refunds to trustees throughout their plan period.

Bankruptcy Discharge and Student Loans

Student loans create the most difficult discharge scenario in bankruptcy law. The conditions for discharging student loans through bankruptcy impose harsh requirements, making discharge extremely difficult but not impossible.

Both federal and private student loans typically survive bankruptcy. Eliminating student loans requires filing a separate lawsuit within your bankruptcy case called an adversary proceeding. This lawsuit demands proving that repayment would create "undue hardship" for you and your dependents.

The undue hardship test varies by jurisdiction, but most courts apply the Brunner test, requiring proof of three elements: First, you cannot maintain even a minimal standard of living for yourself and dependents while repaying loans. Second, additional circumstances suggest this situation will persist throughout a significant portion of the repayment period. Third, you've demonstrated genuine attempts at repayment before requesting discharge.

This test establishes a formidable barrier. Courts have historically denied discharge for people with medical degrees, presuming eventual high earnings, and for younger borrowers, reasoning they have decades to improve financially. You typically need to demonstrate severe, permanent disability, advanced age combined with poverty, or other exceptional circumstances.

Recent policy changes have made student loan discharge slightly more accessible. In 2023, the Department of Justice released new guidance recommending reduced opposition to discharge requests meeting certain criteria. Some bankruptcy courts have begun applying more flexible standards, recognizing that the rigid Brunner test often produces unjust outcomes.

Adversary proceedings add complexity and expense. You must file a complaint, serve the loan servicer and guarantor, and potentially go through discovery and trial. Many bankruptcy attorneys don't handle these proceedings, requiring you to hire additional counsel. Legal fees can exceed several thousand dollars, making this option practical only for borrowers with substantial loan balances.

Some borrowers pursue partial discharge, asking courts to eliminate portions of their student loans while keeping some obligation. Courts have discretion to grant partial discharge when full discharge isn't justified but some relief seems appropriate.

The discharge order is the single most important document in bankruptcy—it's the legal instrument that transforms your financial life. Without proper discharge, bankruptcy provides only temporary relief. With discharge, you get the permanent fresh start that bankruptcy promises, though you must understand its limitations and protect it carefully

— Jennifer Morrison

Common Reasons Bankruptcy Discharge Is Denied

Not everyone who files bankruptcy receives discharge. Courts deny discharges when debtors violate bankruptcy rules or abuse the system. Understanding these pitfalls helps you avoid losing the relief you're seeking.

Fraud tops the list of discharge-denial causes. Filing false bankruptcy schedules, concealing valuable assets, moving property to relatives or friends right before filing, or fabricating financial documents can all trigger trustee or creditor objections to your entire discharge. Even seemingly minor omissions—failing to list a bank account, understating income, or hiding valuable possessions—can result in discharge denial when courts determine you acted intentionally.

The U.S. Trustee's office actively pursues suspected fraud. They cross-reference your bankruptcy schedules against tax returns, bank records, and other documents. Discrepancies trigger intense scrutiny. Finding fraud evidence prompts them to file complaints objecting to your discharge, forcing you to defend yourself through an adversary proceeding.

Author: Victor Langston;

Source: dynamicrangemetering.com

Skipping required courses prevents discharge automatically. Both pre-filing credit counseling and post-filing financial management courses are non-negotiable. Missing either deadline means no discharge. Courts show little tolerance for excuses—the deadlines are clear, and extensions are rarely granted.

Refusing to cooperate with your trustee will sabotage your case. Skipping the 341 meeting, refusing to provide requested documents, or answering questions dishonestly allows trustees to seek dismissal or discharge denial. Cooperation includes producing tax returns, income verification, bank records, and any other financial materials the trustee requests.

Concealing assets proves particularly problematic. Debtors sometimes assume they can hide valuable items—jewelry, collections, cryptocurrency, business ownership interests—by simply not listing them. Trustees have tools for discovering hidden assets, including reviewing social media, searching asset databases, and conducting sworn questioning. Getting caught means losing not just the hidden asset but potentially your entire discharge.

Filing bankruptcy repeatedly within certain timeframes blocks discharge. Getting a Chapter 7 discharge within the previous eight years prevents obtaining another Chapter 7 discharge. Getting a Chapter 13 discharge within the prior six years (with exceptions) blocks Chapter 7 discharge. These timing restrictions prevent serial bankruptcy abuse.

Destroying or creating false financial records triggers discharge denial. You must preserve all financial documentation and produce it upon request. Claiming you've lost records or cannot locate information raises red flags, especially when trustees suspect concealment.

Prior bankruptcy abuse can haunt current proceedings. Filing multiple bankruptcies, dismissing cases to avoid paying creditors, or having a history of bankruptcy-related misconduct causes courts to scrutinize your current case more intensely. Judges remember repeat filers and may resist granting discharge when they suspect system manipulation.

FAQ

Can all debts be discharged in bankruptcy?

No, many debt types survive bankruptcy no matter which chapter you file. Child support, alimony, most student loans, recent tax debts, court fines and restitution, debts from fraud or intentional harm, and debts you forgot to list in your bankruptcy filing remain collectible after discharge. Most credit cards, medical bills, personal loans, and older tax debts typically qualify for discharge.

How long does it take to get a bankruptcy discharge?

Chapter 7 filers typically receive discharge around three to four months after their filing date. Chapter 13 filers must complete their three-to-five-year repayment plan before obtaining discharge, meaning three to five years from filing. Complications like creditor objections, incomplete paperwork, or missing required courses can delay discharge in either chapter.

What is a discharge order in bankruptcy?

The discharge order represents the official court document erasing your personal responsibility for qualifying debts. This order creates a permanent barrier preventing creditors from pursuing collection on those debts. Courts mail copies to you and every creditor listed in your case. Creditors who violate the discharge order through continued collection attempts can face contempt sanctions from the court.

Can creditors contact me after bankruptcy discharge?

Your discharge order permanently prohibits creditors from pursuing collection activities on eliminated debts. When a creditor calls, writes, or sues you about a discharged debt, they're breaking federal law. You can ask the bankruptcy court to sanction the creditor. Creditors can still pursue you for debts that weren't discharged or new obligations you created after filing.

Will I lose my property after bankruptcy discharge?

The discharge itself doesn't cause property loss—property issues get resolved during bankruptcy proceedings before discharge. In Chapter 7, trustees can sell non-exempt property before granting discharge, but most filers keep everything through exemptions. After discharge, creditors cannot seize property to satisfy discharged debts. However, secured creditors keep liens on collateral, requiring continued mortgage and car payments to preserve that property even after discharge.

Can my bankruptcy discharge be revoked?

Discharge revocation can happen, though it's exceptionally rare and must occur within specific timeframes. Courts can revoke Chapter 7 discharge when you obtained it fraudulently and the requesting party didn't discover the fraud before discharge was granted. Revocation requests must be filed within one year after discharge. Chapter 13 discharge can be revoked if you obtained it fraudulently. Courts only approve revocation when presented with clear evidence of serious misconduct.

Bankruptcy discharge is the legal mechanism that makes bankruptcy effective for debt relief. Without discharge, filing bankruptcy would only provide temporary relief from collection efforts. The discharge order permanently eliminates your personal responsibility for most unsecured debts, providing the fresh financial start that bankruptcy laws promise.

The path to discharge differs substantially between Chapter 7 and Chapter 13. Chapter 7 offers quick discharge—typically within four months—but requires passing income qualifications and potentially surrendering non-exempt property. Chapter 13 requires years of plan payments before discharge but allows keeping property and eliminating certain debts that survive Chapter 7.

Not every debt qualifies for discharge. Student loans remain exceptionally difficult to eliminate, requiring a separate lawsuit and proof of undue hardship. Child support, recent taxes, and debts from fraud survive bankruptcy regardless of chapter. Understanding which debts will be eliminated before filing helps you set realistic expectations and choose the appropriate bankruptcy chapter.

Protecting your discharge requires completing every requirement: filing accurate paperwork, attending hearings, providing requested materials, and finishing both mandatory courses. Fraud, concealment, and refusing to cooperate with your trustee can result in discharge denial, leaving you worse off than before filing.

After obtaining discharge, focus on rebuilding credit, maintaining sound financial practices, and understanding your rights. When creditors try collecting discharged debts, they're breaking federal law. Keep records of violations and take enforcement action through the bankruptcy court if needed. Your discharge provides powerful protection—use it to build the stable financial future that bankruptcy makes possible.

Medical bankruptcy helps thousands of Americans eliminate overwhelming healthcare debt each year. This guide explains how bankruptcy discharges hospital bills, which chapter to file, the complete process, costs, and consequences of using bankruptcy to clear medical debt permanently

Bankruptcy stays on credit reports for 7-10 years, but errors happen frequently. Discover how to identify bankruptcy reporting mistakes, dispute inaccurate information with credit bureaus, and rebuild your credit score through proven strategies after bankruptcy discharge

Bankruptcy remains on your credit report for 7-10 years depending on the chapter filed, but its impact diminishes significantly over time. Understanding the specific timeline and taking strategic rebuilding steps helps you recover your credit score and qualify for loans years before the bankruptcy notation disappears

Filing for bankruptcy triggers significant credit consequences, but understanding the specific impact helps you prepare and recover. Chapter 7 stays on your report for 10 years and can drop scores 150-240 points, while Chapter 13 remains for 7 years with a 130-200 point decrease

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to bankruptcy, debt relief, credit rebuilding, and related legal processes.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Bankruptcy outcomes and procedures may vary depending on jurisdiction, personal circumstances, and applicable laws.

This website does not provide legal, financial, or credit advice, and the information presented should not be used as a substitute for consultation with qualified attorneys or financial advisors.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.